Creditas Financial Results Q1-2025

We continue accelerating sustainable growth, balancing gross profit generation and investments in customer acquisition

São Paulo, 29th May 2025

Business Context

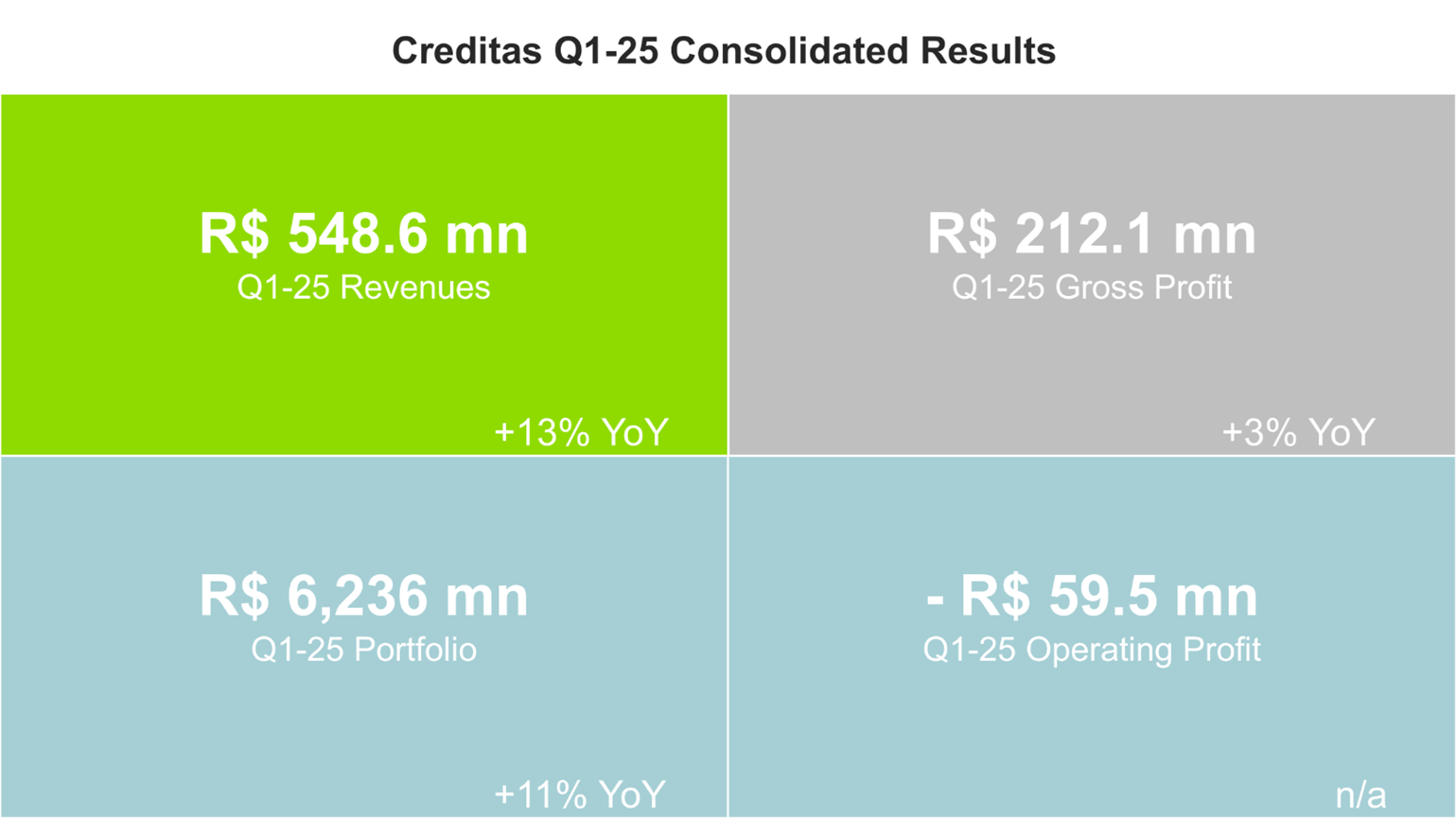

Key Highlights - Q1 2025

Portfolio

Loan origination accelerating despite start of transition to eConsignado where we are having a very conservative approach: R$862.9mn origination (+44.1% YoY and +7.2% QoQ)

Portfolio reaching R$6,236.3mn (+11% YoY and +3.8% QoQ)

Financials

Record quarterly Revenues at R$548.6mn (+13.0% YoY and +3.4% QoQ) as we benefit from increasing volumes and resume portfolio price increase linked to the evolution of interest rates in Brazil

Gross Profit compression to R$212.1mn (+2.9% YoY and -10.4% QoQ) with Gross Profit Margin on revenues at 38.7%, temporary below our 40-45% target reflecting the acceleration of our portfolio with impact in IFRS provision frontloading and increase in Central Bank rates started in Q4-24. Considering the correction for excess provision under IFRS, our Gross Profit is 40.7% and +11.8% YoY

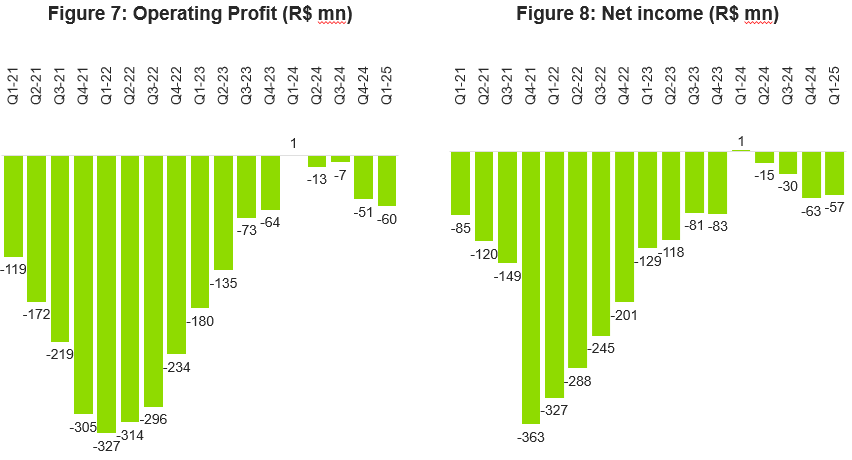

Operating loss of R$59.5mn in line with our expectation, reflecting our investments in growth and frontloading of IFRS provisions, partially offset by increased efficiency in Customer Acquisition Costs

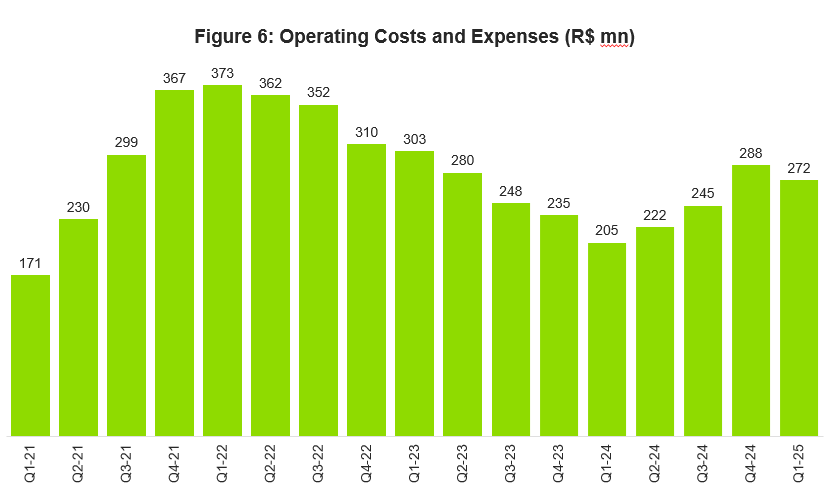

Costs below Gross Profit decreased to R$272mn (-6% QoQ) despite our 7% increase in origination volume as we continue optimizing our user experience, benefit from better seasonality and remain discipline in fixed costs

We continue targeting neutral cash flow as guardrails for our operation since end of 2023, financing growth without the need for external capital

Operations

Gaining significant traction in automation of some of our critical operational processes in Home Equity and Auto products, reaching our highest productivity metrics

Ramping up investments in AI in multiple areas including customer experience, operational processes and coding, while keeping a disciplined approach to return on investments

Started migration of Private Payroll loans to the new Consignado Trabalhador with a very conservative approach as we want to assess the new platform during Q2 and Q3 before ramping up origination

First Quarter Financial & Operating Results

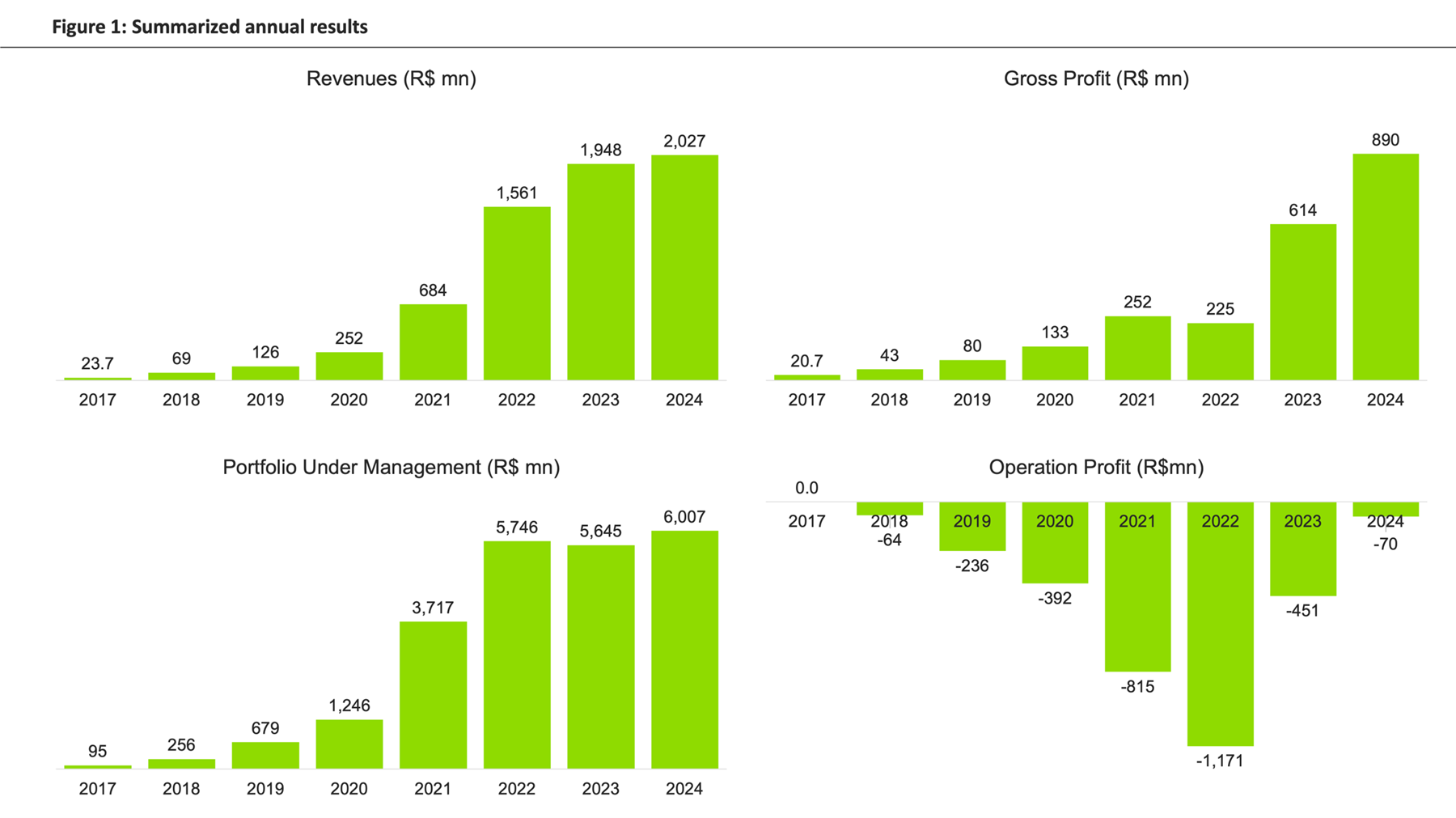

We finished 2024 with margins at peak, record revenues and volumes started picking up in the second half of the year (see Figure 1 with summarized annual results). These results of 2024 will bring growth tailwinds into 2025 and beyond as we keep accelerating our portfolio growth.

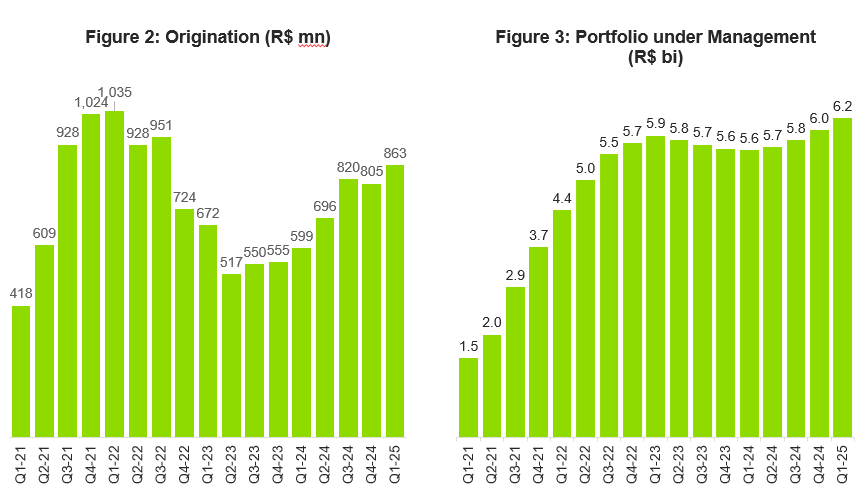

In Q1-2025, we maintained our growth trajectory, prioritizing increased origination of our established Auto and Home Equity products while maintaining cost discipline to avoid capital consumption. Growth continues accelerating with origination +44% and Portfolio +11% YoY (see Figure 2 and 3).

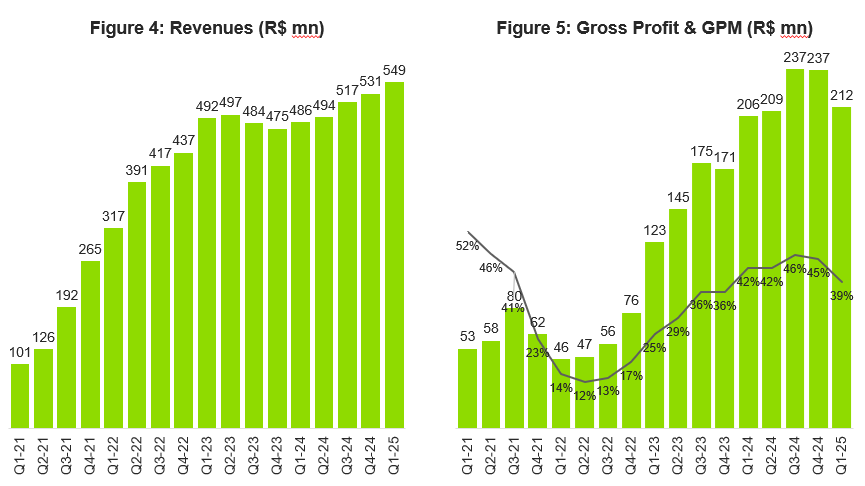

Significant ramp up in origination supported revenues growth to a new record of R$548.6mn in Q1-25 +13% YoY (see Figure 4) while increasing our Cost of Credit. As a reminder, under IFRS we frontload future provisions which creates a significant non-cash impact in gross profit that is not related to credit quality but to growth. The non-cash impact of provisions coupled with the increase in SELIC rates temporarily increases our costs bringing our Gross Profit to R$212mn in the quarter (+2.9% YoY) with 38.7% gross profit margin (See Figure 5). Considering the correction for excess provision under IFRS, our Gross Profit is 40.7% and +11.8% YoY.

Costs below gross profit (see Figure 6) decreased by 6% in the quarter while increasing 32.7% YoY to R$272mn as we raise our investments to boost volumes (+44.1% YoY growth), reflecting improved client acquisition efficiency, operational performance gains, and our continued conservative approach in corporate expenses. It is important to remember that Creditas recognizes all acquisition and technology costs upfront, while loan & insurance margins accrue over time.

We are strategically reinvesting profits to fuel further growth in 2025, supported by strong unit economics and a shorter payback period. Although stronger growth and rise in SELIC has a short-term impact on our cost accounting recognition, we are focused on net present value over short-term profitability as this will build significant cash flows for the future.

In Q1-25 we maintained operating loss at R$60 million (see Figure 7) and net income at R$57 million (see Figure 8), consistent with Q4-24 levels. Despite this operating accounting loss, we have sustained neutral cash flow generation since the end of 2023, enabling us to finance our growth internally without external capital. The performance of this quarter highlights our continued momentum and underscores the strength of our discipline in portfolio expansion, cost control and focus on sustainable, long-term value creation.

Business Unit Performance

Auto Equity

Creditas’ flagship product reached record quarterly originations in Q1-25 driven by strong lead acquisition in the beginning of the year with volumes growing +59% YoY. Continued investments in digital onboarding and customer acquisition are fueling momentum into 2025.

Home Equity

Home Equity continue showing strong momentum despite the softer market, delivering 26% YoY portfolio growth with accelerated traction since the beginning of the year. Focus on streamlining the user experience and lower acquisition cost helped drive growth and expand market share with continued ramp-up of both direct-to-consumer and our affiliate networks.

Private Employees Payroll Loans

Despite the ongoing transition to the new Consignado Trabalhador, the business unit continued to demonstrate growth in Q1-25 with controlled customer acquisition. Since March 2025, we have ceased operating the legacy product and commenced migrating to the new product. We remain very cautious in this transition as we want to ensure full understanding of the risk & rewards of the new platform.

Auto Finance

Stable trajectory as we remain in an exploratory phase. We believe the product has a good fit within the Creditas ecosystem of solutions - multiple initiatives running in parallel to identify the best angle to expand our market share. We are progressively increasing origination as we continue gaining confidence with the product.

Insurance

Continue to scale our insurance operations consolidating Minuto as the leading independent car insurance broker, while bringing the business to profitability. Numerous avenues to explore full potential for insurance within Creditas ecosystem. We continue investing in these fronts during 2025 and expect insurance to become instrumental in the growth of our platform over the years.

Business Outlook

Creditas is in a new growth phase, supported by a foundation of high client recurrence that supports our revenue base, strong credit performance, and clear product-market fit across all core offerings. Investments in user experience and automation will remain priorities in 2025 with AI now delivering tangible value, positioning the company for an annual growth target of 25%+ in the coming years, while maintaining portfolio profitability.

Subscribe for

updates

Receive all our news in your email